Second Waziristan Block Discovery Boosts Gas Supply

April 3, 2026

Pakistan’s energy sector is one of those things that sounds impressive on paper until you actually look at what’s happening on the ground. The country has expanded its installed electricity capacity by 64% since 2013, crossed the 46,000 MW mark, and still somehow manages to leave millions of people in the dark. Literally.

If you’ve ever wondered why your UPS is doing more work than your government, or if you’re an investor or analyst trying to make sense of the sector before putting money in, this breakdown is for you. No jargon walls, no whitewash, just the real picture.

AI Generated Image

Pakistan’s energy sector at a glance

Before you can understand what’s broken, you need to understand what actually exists. And what exists is… complicated.

How much power does Pakistan actually produce?

As of March 2025, Pakistan’s installed electricity capacity standed at 46,605 MW, a 64% jump from where it was in 2013. That’s not nothing. That’s actually a pretty significant infrastructure push over a decade.

Here’s the catch: capacity and delivery are two completely different things. Pakistan regularly faces situations where demand outstrips the power that can actually reach consumers, not because plants aren’t running, but because of distribution failures and the money problems we’ll get into shortly. Around 95% of the population technically has grid access, which sounds great until you remember that 40+ million Pakistanis still live without reliable electricity.

So yes, there’s power. Getting it to people who need it, at a price the system can sustain? That’s the chapter nobody wants to write.

Who runs the energy sector? The key players

Think of Pakistan’s energy governance as a complicated family dinner where everyone has a role but nobody agrees on the menu.

NEPRA (National Electric Power Regulatory Authority) is the regulator, responsible for licensing, setting tariffs, and managing net metering rules as rooftop solar becomes a bigger part of the picture. WAPDA, which used to be the dominant player in electricity, has been restructured into 10 distribution companies and 4 generation companies. NTDC (National Transmission and Despatch Company) manages the national grid at 500 kV and 220 kV levels, basically the motorway of electricity.

Then you have PPIB (Private Power and Infrastructure Board) and AEDB (Alternative Energy Development Board), which exist to facilitate private and renewable energy investment. In theory, a well-oiled machine. In practice, a system where coordination failures cost billions.

How is electricity distributed in Pakistan?

This is where things start to get interesting, and by interesting, we mean occasionally infuriating.

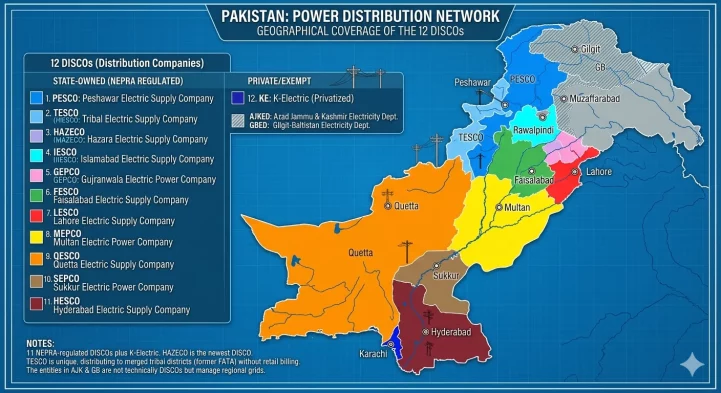

The 12 DISCOs: Pakistan’s distribution network

Outside of Karachi, Pakistan’s electricity distribution is handled by 12 Distribution Companies, or DISCOs. These cover every province and region, from IESCO in Islamabad to HESCO in Hyderabad to QESCO in Quetta. Each DISCO is a government-owned entity responsible for getting electricity from the grid to your home or business.

Karachi is the one outlier. K-Electric operates as Pakistan’s only privately-owned utility, managing generation, transmission, and distribution for the city all on its own. K-Electric has its own set of problems, but it’s structured fundamentally differently from every other distribution company in the country.

The DISCOs’ big problem? They routinely report aggregate technical and commercial (AT&C) losses exceeding 20% of the power they receive. Global benchmarks for efficient utilities hover around 3-5%. Losses at that scale aren’t just a technical issue, they’re a financial black hole that the whole system eventually falls into.

AI Generated Image

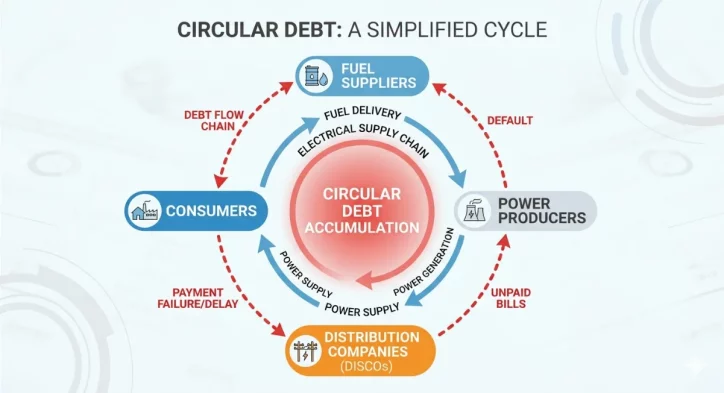

The circular debt crisis: why it matters to you

You’ve probably heard the phrase “circular debt” thrown around in headlines about Pakistan’s economy. Here’s what it actually means in plain terms.

The circular debt in Pakistan’s power sector had ballooned to over Rs2.6 trillion (roughly $9.3 billion) as of mid-2025. It works like this: DISCOs can’t recover the full cost of electricity they distribute because of theft, technical losses, and consumers who don’t pay. Because they can’t collect enough, they can’t pay generation companies. Generation companies can’t pay fuel suppliers. Fuel suppliers stop supplying. Power plants slow down. Outages happen. Rinse, repeat.

What makes it worse is that some of the biggest defaulters on electricity bills are provincial and federal government agencies themselves. Your tax money is, in part, subsidizing the government’s own failure to pay its electricity bills. The irony writes itself.

AI Generated Image

Is Pakistan’s energy sector private or government-owned?

Short answer: both, and the split is messy.

The public vs. private split

On the generation side, Pakistan has over 36 Independent Power Producers (IPPs), private companies that built power plants and sell electricity to the government under long-term agreements. As recently as 2016, IPPs were generating 53% of the country’s total electricity output. That’s a majority of the grid in private hands.

On the distribution and transmission side, the government owns everything except K-Electric. All 12 DISCOs are state-owned, and so is NTDC. So the model looks like this: private companies generate electricity, sell it to the government, and the government’s companies distribute it, often inefficiently, to consumers.

The IPP problem: paying for power nobody uses

Here’s where the policy chickens of the 1990s have come home to roost. When Pakistan signed agreements with IPPs in the 1990s and early 2000s to attract private investment into power generation, those contracts included “capacity payments,” meaning the government pays IPPs whether or not their electricity is actually consumed.

The logic made sense at the time. You need to attract investors, so you guarantee them revenue. Fast-forward to 2025, and you have a situation where rooftop solar adoption is pulling consumers off the grid, reducing demand, but the government still owes full capacity payments to IPPs regardless. Fewer consumers on the grid means those fixed costs are distributed across a shrinking base of paying customers, which drives tariffs up, which pushes more people toward solar, which shrinks the base further. A very 21st-century spiral.

To its credit, the government actively renegotiated IPP agreements in 2025 to reduce the capacity payment burden. Whether those renegotiations succeed at the scale needed is a different question.

Can Pakistan produce enough energy?

Technically, yes. Sustainably? Not yet.

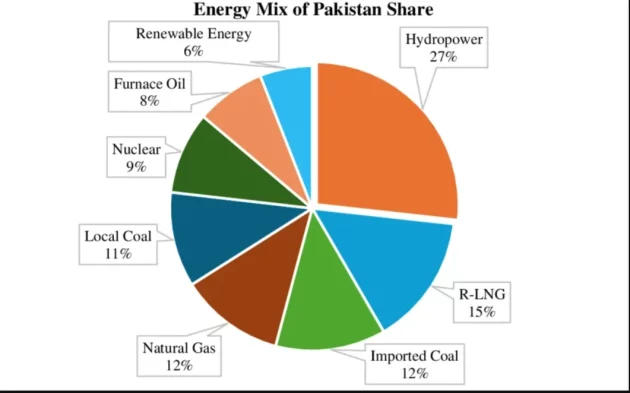

Generation mix: what’s powering the grid right now?

Pakistan’s electricity generation is dominated by fossil fuels, and not even cheap ones. RLNG (re-gasified liquefied natural gas) and local gas together account for about 40% of generation. Imported coal adds another 16%, and oil another 16%. The import dependency in that mix is significant, especially for a country that has repeatedly faced foreign exchange crises.

Renewables are growing but still account for a minority of the generation mix. Hydro contributes around 4%, wind about 7%, solar 3%, and bagasse (sugarcane residue) roughly 1%. For a country with some of the best solar irradiance and wind corridors in Asia, the renewable share is underperforming the potential.

Pakistan has set a target of 60% renewable electricity by 2030. Given where the mix stands today, that’s an ambitious climb. But the direction of travel is right.

Energy mix of Pakistan in 2023 in MW and percentage share by Atique u Rehman

Load shedding in 2026: still a problem?

Unfortunately, yes. Here’s what makes it maddening: Pakistan has excess generation capacity on paper. The system isn’t short of power plants. It’s short of the infrastructure to move and deliver that power reliably.

Aging distribution infrastructure, transformer overloads, and consistent under-investment in grid maintenance mean that even when power is being generated, it doesn’t always make it to end users. AMI (Advanced Metering Infrastructure) is being rolled out to help tackle technical and commercial losses, which is a step in the right direction. But infrastructure upgrades take time, and Pakistan’s distribution network has years of deferred maintenance to catch up on.

What’s next: privatization and reform

This is the part of the story that will define the next decade for Pakistan’s electricity sector.

5 DISCOs on the privatisation block

Under conditions tied to the IMF’s ongoing program with Pakistan, the government has shortlisted five DISCOs for privatization: IESCO, FESCO, GEPCO, HESCO, and SEPCO. The rationale is straightforward: private operators with commercial incentives and harder budget constraints should, in theory, reduce losses, improve billing recovery, and take the financial pressure off the federal government.

QESCO (Quetta Electric Supply Company) and TESCO (Tribal Electric Supply Company) have been excluded from the current round due to security concerns and structural constraints in the regions they serve.

Whether DISCO privatization delivers on its promise depends almost entirely on the regulatory framework and whether new owners are given the operational latitude to make real changes. Without that, you’re just transferring losses from a public entity to a private one.

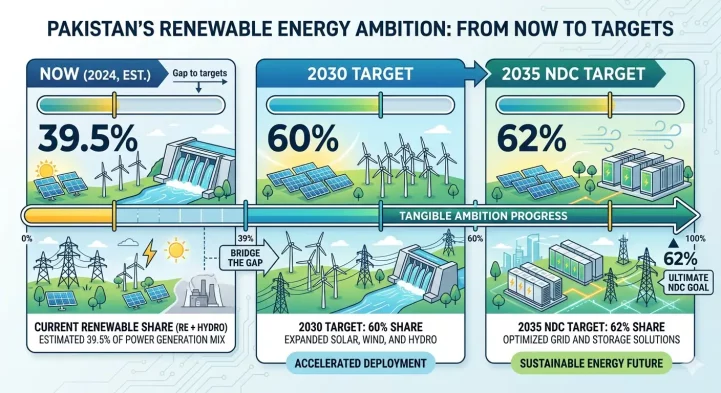

Pakistan’s renewable energy targets

The solar story in Pakistan is genuinely one of the more exciting things happening in the sector. In 2024 alone, an estimated 17 GW of solar capacity was added, driven largely by private household and commercial adoption. Pakistan’s NDC (Nationally Determined Contribution) commits to reaching 38.5 GW of renewables capacity by 2035, which would put renewables at 62% of the total electricity mix.

There’s a complication, though. The government introduced a 10% import tax on solar panels in 2025. For middle and upper-income households, that’s a manageable friction. For lower-income households who could benefit most from off-grid or distributed solar, it’s a real barrier. A policy designed to boost local manufacturing could end up slowing adoption among the people who need it most, at least in the short term.

The renewable energy ambition is real. Getting the enabling policy environment right is the hard part.

AI Generated Image

Conclusion

Pakistan’s energy sector is a study in contradictions. Record installed capacity, chronic outages. Private generation, state-owned bottlenecks. Ambitious renewable targets, coal import dependency. A sector that was reformed in the 1990s and is now being reformed again because the first round created problems that compound interest can’t solve.

The good news is that the direction of travel in 2026 is clearer than it has been in years: renegotiate IPP contracts, privatize the most viable DISCOs, accelerate renewables, and fix the circular debt spiral before it crowds out every other fiscal priority. The hard news is that executing all of that simultaneously, in a politically complex environment, is genuinely difficult.

For investors, analysts, or anyone with a stake in how this plays out: this is a sector in active transition, which means it’s full of both risk and real opportunity. Keep watching.

Key takeaways: Pakistan energy sector stats at a glance

|

Metric |

Figure |

| Installed capacity (2025) | 46,605 MW |

| Capacity growth since 2013 | +64% |

| Population with grid access | ~95% |

| People still without electricity | 40+ million |

| Circular debt (mid-2025) | Rs2.6 trillion (~$9.3B) |

| DISCO losses (AT&C) | 20%+ |

| IPPs in operation | 36+ |

| Fossil fuel share of generation | ~72% |

| Renewable target by 2030 | 60% |

| Solar capacity added in 2024 | ~17 GW |

| NDC renewable target by 2035 | 38.5 GW (62% of mix) |

| DISCOs slated for privatization | 5 (IESCO, FESCO, GEPCO, HESCO, SEPCO) |

{kind=link}

{kind=link}